Blogs

A Systems Approach to Value for Money: Why the Government needs an Effectivity Screen

No amount of poetry

Will mend this broken heart

But you can put the Hoover round

If you want to make a start

- Billy Bragg, ‘The Short Answer’ (1988)

The combined Financial Conduct Authority (FCA) and Pensions Regulator (TPR) Value for Money (VfM) consultation for Defined Contribution pensions represents a pivotal moment for UK pension policy - and by proxy the outlook for growth and investment in our country.

While legislators are engaged with the ‘poetry’ of The Pensions Schemes Bill, the three regulators are already at work. They are, in fact, already “putting the Hoover round” as Billy Bragg would say.

For too long, pension scheme governance has operated in a fog of opacity, with members unable to assess whether their retirement savings are being managed effectively. The proposed VfM framework promises to establish transparency and accountability, create systemic incentives for productive capital allocation which actually moves the dial on UK growth, and develop metrics that reveal hidden cost extraction. These outcomes align directly with the Government's objectives of pension system reform and long-term capital mobilization.

At New Capital Consensus (NCC), we welcome this initiative as a significant step toward a proper systems approach —one that relies on incentives and structural levers rather than blunt regulatory mandates.

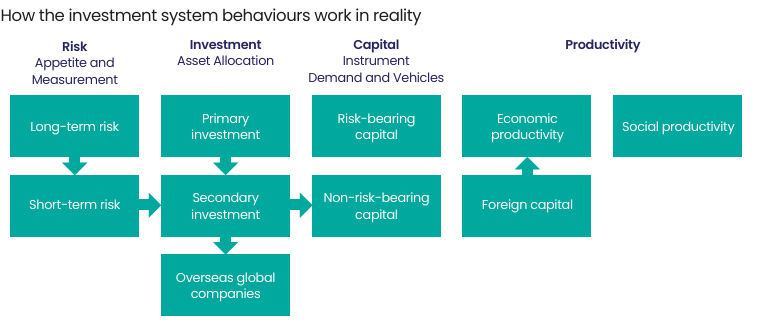

In the course of its qualitative research, NCC itself found no incentives to provide good returns to investors within the dynamics of the system. Rather than focusing on investor returns, NCC found system actors focusing solely on their own liabilities (often shaped by regulation) or commercial pressures or reputational scrutiny.

Putting the Hoover round….

What distinguishes this consultation is its recognition that meaningful reform requires changing the behaviour of actors across the entire investment chain, not simply imposing new rules. By establishing forward-looking benchmarks and comparative frameworks, the VfM regime has the potential to nudge trustees, asset managers, and platforms toward better outcomes for members and the UK economy through aligned incentives rather than compliance obligations.

Each silo of the chain is performing its role as set out in regulation admirably, but to paraphrase Peter Drucker, there is surely nothing quite so useless as doing with great efficiency what should not be done at all.

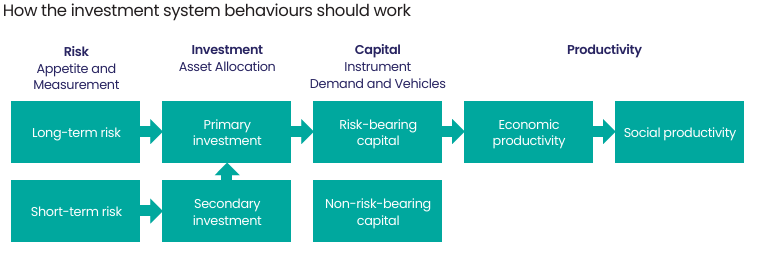

Again, NCC analysis supports the key role that Asset Owners (DB and DC scheme operators) play in setting the tone of the investment chain that also contains Asset Allocators (the managers the pension schemes employ) and Capital Markets (to whom managers turn for appropriate capital instruments). We found that poor risk appetites set by Asset Owners at the start of the investment chain run through the chain like letters in a stick of rock - which hampers the ability of the system to provide positive outcomes for the both UK economy and pensioners.

… but only to make a start

However, there is a significant risk that the emerging framework will be neutered by regulatory compromise and unresolved technical design flaws.

Critical issues remain unaddressed within the simplistic and one-dimensional traffic light proposal from the FCA including:

- Vague service quality metrics that schemes can easily game.

- A backward-looking focus on costs and past performance rather than forward-looking governance quality.

- The absence of central data architecture; comparator groups that risk creating regulatory herding.

- Unclear bulk transfer mechanics that fail to protect members during consolidation.

The convergent danger is that VfM becomes a compliance checkbox rather than a genuine accountability mechanism—trustees report metrics with little predictive value, regulators lack data to detect problems, and members receive "VfM certificates" that mean nothing.

The NCC Effectivity Screen – mending the system’s broken heart

To address these shortcomings, NCC has developed the Effectivity Screen —a diagnostic framework embedded in our broader Effective Investment research that operationalizes forward-looking VfM assessment.

The Screen interrogates capital allocation strategies across five critical dimensions:

- Right-Sized Risk Perspective: Do your risk assumptions match your members' actual long-term investment horizons, or are you confusing short-term volatility with genuine investment risk?

- Right-Sized Risk Metrics: Does your measurement system accommodate long-term investment, or does it force unnecessary short-term trading behaviour?

- Right-Sized Domestic Allocation: How much capital is invested in UK markets versus overseas, and has this been optimized for member outcomes and UK economic productivity, or is it passive adherence to global indices?

- Right-Sized Primary Allocation: What proportion of capital flows into primary investment (new issuance, infrastructure, innovation) versus secondary market trading of existing securities?

- Right-Sized Risk-Bearing Capital: How much is allocated to genuine risk-bearing capital that matches member time horizons versus defensive assets that provide false comfort?

Leaping Forward

By embedding the Effectivity Screen into VfM reporting, trustees would be required to transparently articulate and defend their allocation philosophy. This transforms VfM from a backward-looking cost exercise into a forward-looking governance discipline—revealing whether schemes are truly serving member interests and contributing to UK productivity.

The consultation window closes on the 8th March . The opportunity to shape the discussion on a genuinely effective VfM framework—one grounded in systems thinking and forward-looking assessment—is now. The detail of the primary and secondary legislation and how VfM is determined will be critical in directing effective investment into the UK and delivering for both savers and society.

Billy Bragg also put his finger on the stop-start nature of politics in 1988: “Well, one leap forward, two leaps back / Will politics give me the sack?” The government’s focus on value-for-money is a clear step in the right systemic direction. But we still need more political focus if we are to make our own “great leap forwards” as an industry in the service of citizen-savers and the UK economy.

We stand ready to work with policy makers to help ensure that these reforms really hit their target, and all the measures in the Pension Schemes Bill can work together to realise the Government's overall goals for pensions saving and the UK economy.

Please login or register to leave a comment on this post.